Materiality Assessment

The Company conducts an annual review and analysis of material sustainability issues relevant to its business and stakeholders. This assessment evaluates both the impacts the organization has on external parties and the impacts external factors may have on the organization.

This process follows the Double Materiality Principle in accordance with international sustainability reporting standards and covers the following two dimensions:

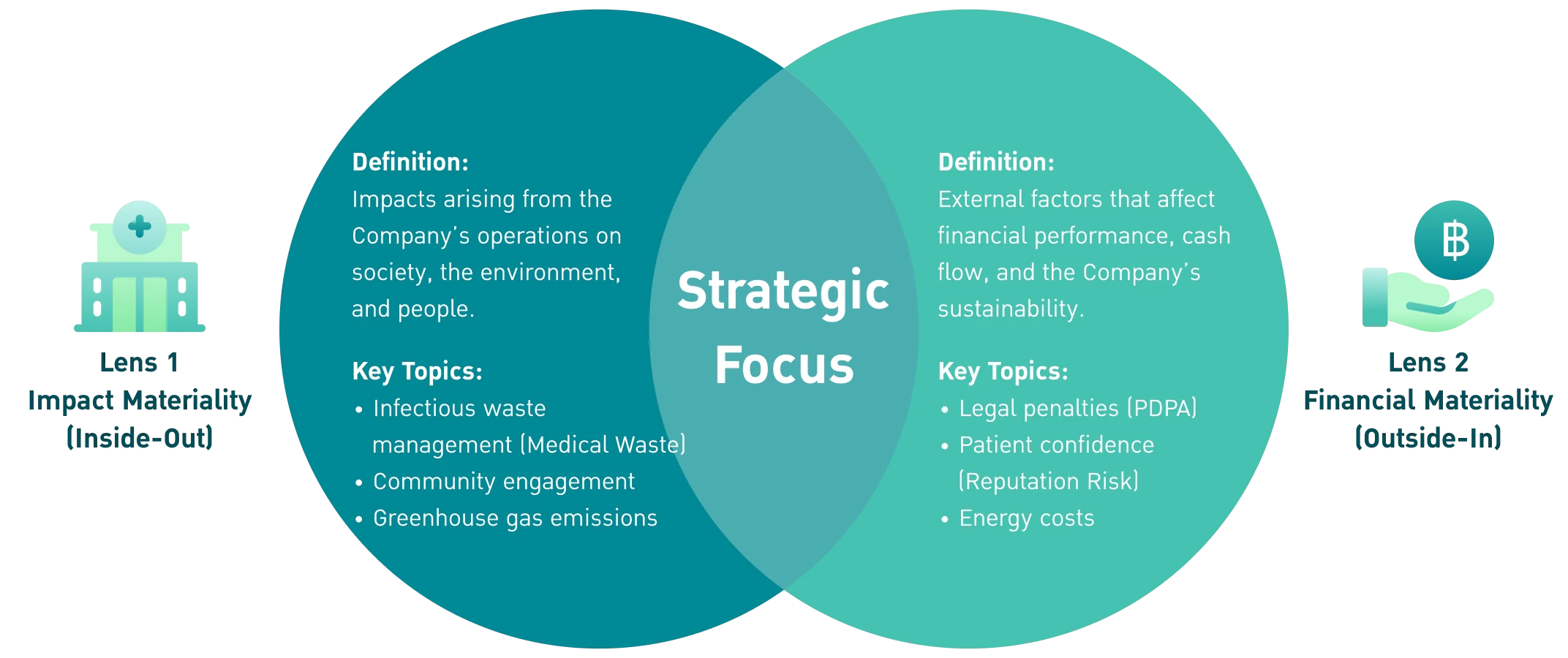

- Impact Materiality: This dimension assesses the impacts of the Company’s activities on the economy, society, the environment, and stakeholders (inside-out perspective), including both actual and potential impacts. For example, initiatives to reduce medical waste may contribute to reducing pollution in surrounding communities, generating actual or potential positive impacts on environmental, social, governance, and economic dimensions.

- Financial Materiality: This dimension considers sustainability-related risks and opportunities arising from external factors that may affect the Company (outside-in perspective). These factors may influence enterprise value, business operations, growth, and financial position. Examples include risks from increased costs due to carbon tax regulations, or opportunities from digital innovation that may enhance revenue generation and strengthen the Company’s business performance and financial standing.

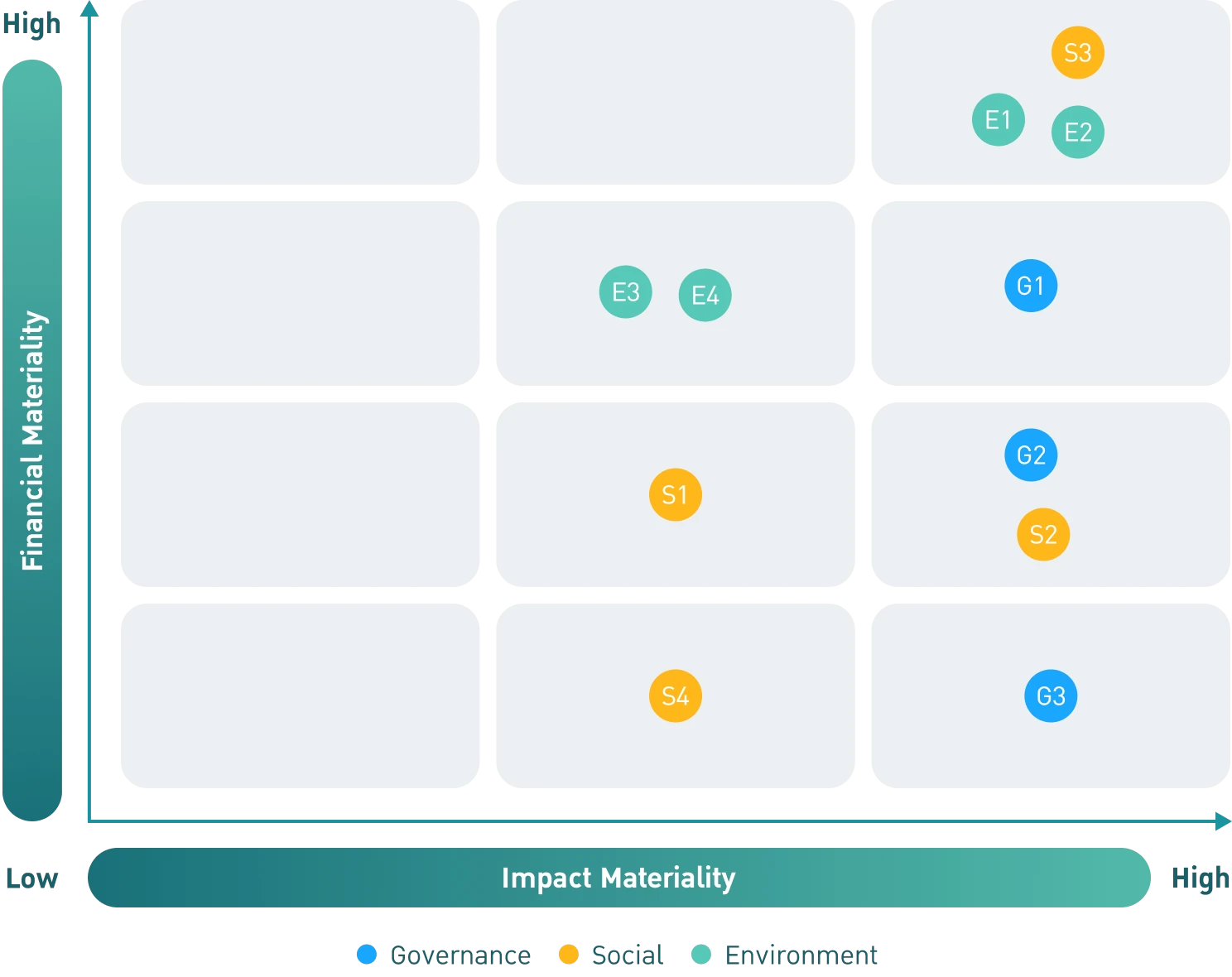

Preliminary material issues are presented in a Materiality Matrix, illustrating the relationship between significant impacts across the two dimensions. The assessment results are reviewed by senior executives serving on the Sustainable Development Working Group and the Corporate Governance and Sustainable Committee before being submitted to the Board of Directors for approval.

Sustainability assessment through two key dimensions to identify factors that genuinely impact “corporate value” and “stakeholders.”

Materiality Assessment Process

Identification

The Company conducts a comprehensive analysis of both internal and external factors, including the following:

- Internal factors (Inside-Out): The Company’s business strategy and direction across the short, medium, and long term, as well as the identification of impacts that the Company’s activities may have on the economy, society, and the environment.

- External factors (Outside-In): Expectations of the six key stakeholder groups gathered through surveys and engagement processes, together with monitoring of international regulations and standards, such as IFRS S1 and IFRS S2, which may affect sustainability-related financial risks and opportunities.

The outcome of this process is a consolidated list of all potentially significant sustainability issues (Long List).

Prioritization

The Company evaluates the issues identified in Step 1 in accordance with the Double Materiality Principle as follows:

- Impact Materiality: Assess the level of impacts (scale, scope, and irremediable character) that the Company has on external parties across economic, social, environmental, and governance dimensions, with reference to the GRI Standards and GRI Sector Standards.

- Financial Materiality: Assess the level of sustainability-related risks and opportunities arising from external factors that may affect the Company’s enterprise value, financial position, and business operations.

The outcome of this process is a prioritized list of material sustainability issues (Short List).

Validation

The Sustainable Development Working Group, together with senior management, conducts a validation of the identified material issues to ensure that they comprehensively reflect the Double Materiality principle, as follows:

- Review the interconnections between internal and external impacts to ensure completeness across both dimensions.

- Present the assessment results to the Corporate Governance and Sustainable Committee for consideration prior to submission to the Board of Directors for approval.

The outcome of this process is a refined list of material sustainability issues (Short List) that have been filtered and validated across both materiality dimensions.

Integration into Strategy, Communication, and Reporting

The approved material sustainability issues are integrated into the Company’s enterprise-level management processes as follows:

- Strategy Formulation: Integrate material issues into the strategic planning process in the fourth quarter to define targets, action plans, and resource allocation.

- Management Implementation: Assign clear accountability for each material issue to designated responsible persons to ensure effective and tangible execution.

Communication and Reporting: Communicate performance outcomes to stakeholders and disclose information transparently in the Form 56-1 One Report and the Sustainability Report.

Material Issues and Impact Boundaries on Stakeholders

| Material Issues | Impact Boundaries | SDGs | |||||

|---|---|---|---|---|---|---|---|

| Internal | External | ||||||

| Employees | Shareholders and Investors | Customers | Suppliers | Communities and Society | Competitors | ||

| Governance and Economic | |||||||

| Corporate Governance and Business Ethics |

|

||||||

| Innovation Development |

|

||||||

| Supply Chain Management |

|

||||||

| Social | |||||||

| Human Rights and Labor Practices |

|

||||||

| Community Engagement |

|

||||||

| Responsibility to Customers |

|

||||||

| Talent Attraction and Personal Retention |

|

||||||

| Environmental | |||||||

| Climate Change Adaptation |

|

||||||

| Energy Conservation |

|

||||||

| Water Management |

|

||||||

| Waste Management |

|

||||||

PR9 Double Materiality Matrix